How to Calculate Your Net Worth

Your net worth is a great (and important) number to understand. It is a snapshot in time showing you how well you are doing financially. The good news is that it is rather easy to calculate too. All you need is a sheet of paper (or a spreadsheet) and some information about your finances. Even if you aren’t very organized, the entire process should take you 20 minutes in all to complete. Here is how you calculate your net worth and why.

How to Calculate Your Net Worth

How to Calculate Your Net Worth

The formula for calculating your net worth is relatively easy. In fact, it’s basic subtraction (with a little addition in there too). Here is how the formula looks:

ASSETS – LIABILITIES = NET WORTH

That’s it! To complete the calculation you add up all of your assets and all of your liabilities and then subtract to get your result. What all makes up assets and liabilities? Glad you asked!

Assets

Assets include many things. Think cash, bank account and investment accounts as starters. This includes any retirement money you have too. From there, you have to include other assets you might have – like a car, a house, furnishings, collectibles, etc.

While it is easy to value your bank accounts, your collectibles, furnishings and clothing might be a little tougher. In these cases, your best option is to add everything up and then lower that amount by 50% (or cut in half) to get to a number. This is done because we tend overestimate the values of things, mainly for sentimental reasons.

For your car and house, you can use guides like Kelly Blue Book for your cars estimated value and Zillow for your house.

Liabilities

Liabilities include all loans you have. So your home loan, auto loan, credit card debt, student loans, etc. would all be included here. Luckily this part of the calculation is easy to figure out since you have statements to work off of to get the current loan numbers.

Performing The Math

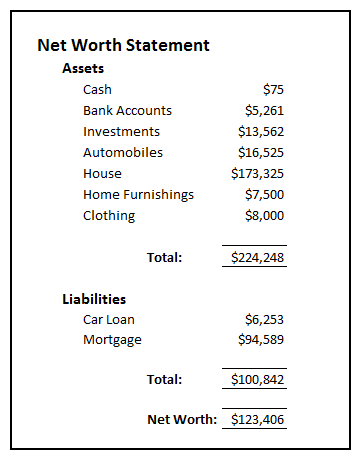

Once you have everything, you need to organize it all. Here is a sample of a net worth statement I created:

As you can see, I have assets listed first as well as their values. The last line is the total assets I have. Below that I have all my liabilities and again, they are all totaled at the end. From there, it is simply taking assets minus liabilities to get to my net worth. In this case, my net worth would be $123,406.

(A few notes: you can get as detailed as you want with your net worth statement. For example, I just listed bank accounts as one entry. This includes both my checking and saving accounts. You can do the same or break them out so you can see each one. Breaking them out does make it easier to see the changes over time.

Also, some people include their primary house in their net worth, while others do not. Here is a good article about the topic. If you decide to keep it out, make sure you keep it off of both sides of the equation.)

Read More: What Percentage of Assets and Liabilities are in Your Home?

What Your Net Worth Tells You

So why exactly should you calculate this number? As I mentioned earlier, it gives you a nice snapshot of how you are doing financially. If you have a negative net worth, meaning you owe more than you have, it “could†mean you need to pay down debt and start living within your means.

I say “could†because if you are young, you probably have a negative net worth. This is because you really haven’t had the time to earn a decent amount of money and you could have student loans. But as you get older, your net worth should certainly turn positive and continue to grow as you earn more and eliminate your debt.

Read More: What Should Your Financial Pie Chart Look Like?

Comparing Net Worth

Many people want to know how they compare to others in terms of net worth. This is usually a pointless endeavor. The reason for this is because no two situations are alike. A person living in New York City is going to have a vastly different net worth than someone living in Texas. Housing prices are too different as are salaries. So just because someone else your age has a much higher net worth, it doesn’t mean you aren’t doing as well as you should.

You should have your own goals and targets for growing your net worth and update your numbers annually. For me, I like to grow my net worth by around 10% per year. This is done both by paying down debt and saving money every month.

Read More: Are You Focused on Today or Tomorrow?

Final Thoughts

Take the time to calculate your net worth. It is an easy calculation to make and it will show you just how well you are doing financially. I encourage you to calculate it with an open mind the first time, and then make it a point to increase it every year by a certain amount. Start off with 5% and work towards 8-10% per year. If you can do this, you will find that in time, you will be debt free and have a nice sized nest egg to retire on and enjoy more experiences in life.

More Finance Topics

- What is the Rule of 72?

- How to Calculate Internal Rate of Return on Your Investments

- 7 Passive Income Ideas to Make Extra Money

- 6 Successful Ways to Save Money This Year

- How to Put More Money in Your Savings Account

- 5 Keys to Becoming a Millionaire

- Why You Should Save 1% More Each Year

- How to Make Sense of Interest Rates, APYs and APRs

What about using life insurance as part of your net worth calculation? I have seen people say yes, I have seen people say no. What if it is your life insurance? What if it is a parents life insurance you are named on?