What Percentage of Assets and Liabilities are in Your Home?

If you are familiar with business finance at all, you know that a company’s balance sheet lists its assets and liabilities, for a point in time. It is basically a snapshot of the company on a given date. You as a consumer also have a balance sheet. Most people refer to their balance sheet as their net worth statement because when you subtract your liabilities from your assets, the resulting number is your net worth. Similarly, if you were to do the same with a company’s balance sheet, you would find the owner’s equity of company.

Assets and Liabilities

As you move along in life, your gain assets and take on some liabilities. Ideally, you take on the least number of liabilities possible. But as you move along, you never know how you compare to others. Below is the average consumer’s balance sheet. It lists what makes up each side of their ledger, assets and liabilities. Realize that the goal is not for you to compare your situation with these numbers to figure out if you are ahead or behind. This is more for informational purposes. Because of this, I only present the information in percentages, so that net worth cannot be determined. If you are interested in net worth, see Net Worth by Age.

Assets

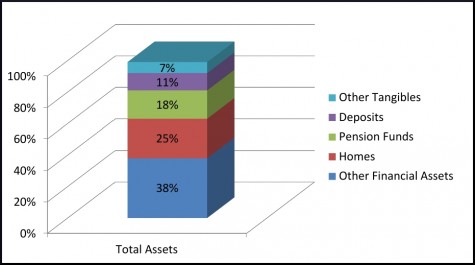

Percentage of assets in home. As you can see, housing makes up 25% of the average consumers assets. Knowing this helps you to realize why so many people are in financial disarray currently. With the drop in home prices and the high percentage of assets in home, a majority of their assets have been wiped out.

Pensions and investments make up 56% of assets. This includes all investment accounts: 401(k), IRA, Roth IRA, etc., as well as non-retirement investment accounts. This includes brokerage account and bank accounts.

All of the average consumer’s tangible assets, such as clothing, automobiles, household items, etc., account for 7% of their assets.

Liabilities

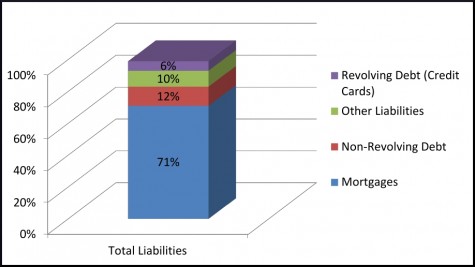

Percentage of liabilities in home. On the liabilities side, mortgages make up 71% of the average consumers liabilities. Comparing this with the fact that 25% of the average consumer’s assets are their homes, we can see a few things: either people have large outstanding loans compared to equity in their houses or they have very large amounts of other assets, driving down the percentage that their homes make up.

Credit card debt totals 6% of liabilities and other non-revolving loans, such as auto loans, student loans, etc. make up 12%. While on the surface this looks encouraging, it can be misleading. Since outstanding mortgages tend to be large, as in hundreds of thousands of dollars, credit card debt, auto and student loans will naturally have a smaller percentage.

For example, if the average debt is $350,000 (I’m making this up for illustration purposes), that means $250,000 is mortgage debt (71%). Credit card debt, which is 6%, would be $20,000 in this case. That is a high amount.

Finally, all other liabilities make up 10% of the average consumers balance sheet.

Final Thoughts

The average consumer’s balance sheet can tell us a lot. But it also forces us to look deeper to get a true picture of the health of the balance sheet. The takeaway from this should be one that many personal finance experts try to hammer home: build up your assets while taking on little or no debt. Save up for as much of a down payment as possible. The less liabilities you have, the better able you will be to weather any storms.