If you’re over 50 and diligent about retirement savings, you may be maxing out both your 401k and traditional or Roth IRA [1].

But to really supercharge your savings and make sure you are extra-prepared for retirement, you should also take advantage of catch up contributions. Catch-up contributions are special provisions that allow you to contribute additional funds to your retirement accounts as you get closer to retirement. This has the double benefit of helping beef up your retirement savings while deferring taxes.

Why Catch Up Contributions Matter

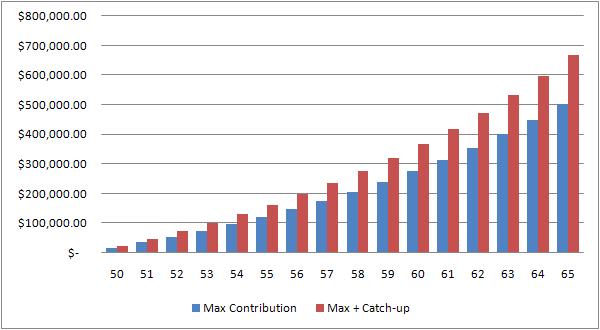

Here’s a graph showing someone who started maxing out a 401k five years ago with an 8% earnings rate; he or she would save just over $500,000 between ages 50 and 65. Someone taking full advantage of catch-up contributions would save over $667,000 in that same time period. (The contribution limits and catch up limits have gone up over the past few years so the numbers would be a slightly higher if you reran the same scenario today.)

{kind=link}

If you withdraw 4% [2] of your nest egg annually in retirement, that additional savings would mean an additional $6,000 of income per year.

Over 50 Catch up Contribution Limits

Most retirement accounts allow for additional contributions for account holders over 50. Here are the updated 2015 limits:

- 401(k), 403(b), 457: May contribute $6,000 above the limit [3] of $18,000 in 2015 for a total of $24,000. Remember that the 401k catch up limit applies to the total of all 401k and 403b accounts held by one employee, even across multiple employers. 457 accounts have a separate $24,000 limit.

- Traditional IRA/Roth IRA: Up to $1,000 above the standard $5,500 maximum Roth contribution [4] in 2015.

- SIMPLE IRA [5]: Up to $3,000 above the standard $12,500 in 2015.

403b 15-year Catch-up

If you have 15 years of service with a public school system, hospital, home health service agency, church, or certain other organizations, you can increase your 403(b) contributions by the lesser of:

- $3,000

- $15,000 reduced by previous catch-up contributions (pre-tax and Roth) under this rule

- $5,000 times the number of years of service minus total contributions made in earlier years

The IRS explains further [6]. Note that this applies to all employees with 15 years of service at a qualified organization, regardless of age. If you are over 50 you may take this AND the over-50 catch-up noted above.

457 Double Limit Catch-up Contribution

In the three years before normal retirement age (as defined in plan document), government and certain non-government employees may take what’s known as the “double limit catch-up [7].†If you did not contribute the maximum possible amount in previous years, you can contribute double the current year’s maximum amount OR the sum of “missed†contributions in previous years.

If you take this catch-up you cannot take the over-50 catch-up for 457s.

Take Action

If you want to increase your retirement savings, log in to your online account or contact your benefits coordinator at work.