Are You Still Using Lending Club?

It’s been awhile since we’ve done a Lending Club update. If you’re not familiar, Lending Club is a peer-to-peer lending service. Regular people like you and me can use the site to borrow and lend money without using a bank. To run the service, Lending Club charges each party a small fee. But in general, borrowers pay lower interest rates and lenders earn higher interest rates than they would using traditional borrowing and/or investment channels.

My Lending Club Experience

I was a fairly early investor in Lending Club – I made my first loan in 2008. Then the site closed to complete SEC registration. When it reopened, I stayed on the sidelines for a bit. But in early 2009 I couldn’t help myself and became a regular investor. I tended to invest in 1-2 notes a paycheck, for a total of about $1000 a year. I also reinvested all payments I received from the site. At one point, my selective lending criteria was earning me about 10% a year on a total investment of about $3,500.

When I first started investing, I invested in mostly A and B loans. But I found that the interest rates were so low that even one default really drove down my total return. LazyMan discovered the same thing – and just like him, I decided to up my risk in the hopes of increasing my return. It worked for a while – but over time, a larger number of loans defaulted, and my return went back to hovering somewhere around 4-6%.

Around that time, I decided that I wanted to aggressively attack the remains of my student loan debt. Because the interest rate on that loan was above 6%, using funds to invest in new Lending Club loans was not really the best use of my cash. So I stopped adding new money, and began to withdraw much of what I earned. In the meantime, more of my loans went bad.

My Account Today

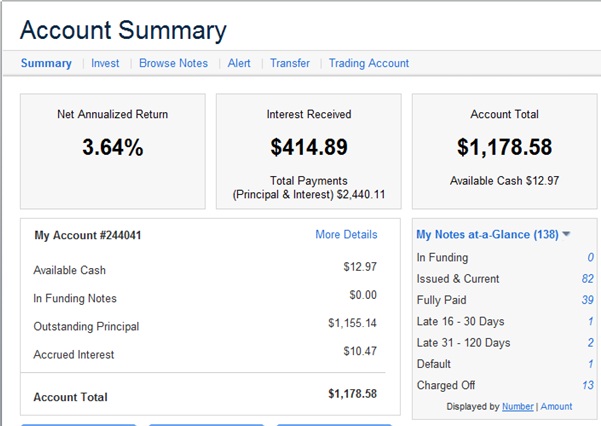

My current account summary

My Lending Club account currently shows a Net Annualized Return of 3.64% – not bad considering the number of defaults I’ve had, but not great. I receive about $80/month income off of my $3500 investment – but that amount is decreasing as some loans reach maturity. All told, a full 10% of my loans have been charged off, and several more look to be headed that way. What’s frustrating is that there doesn’t seem to be a rhyme or reason to the charge-offs – they come from borrowers with different credit scores, incomes and types/amounts of loans. Because of this, my defaults aren’t a good indicator of what to stay away from in the future.

My Future with Lending Club

I’ve made only a few loans in 2012. I currently withdraw most of the money I receive in payments every couple of days, using it to pay down the (nearly non-existent!) remains of my student loan and save for my next big expense. If I ever happen to log in and have over $25 sitting in my account, I do use it to buy a new loan. I’m not adding any new money to my account right now, but I still haven’t quite been able to give up investing altogether!

I’m anticipating that the next year of my life will be among the most expensive I’ve had. Steady cashflow is vital, which doesn’t leave a lot of room for “fun” investments like Lending Club. But when the dust settles and I find myself with a little extra cash on hand, I do plan to dive back in. While Peer-to-Peer lending may not be quite as trendy as it was a couple of years ago, I do believe it’s here to stay. As Lending Club continues to fine-tune its lending process, returns should only improve. I currently have 138 notes, so even one default significantly impacts my returns (my mom has a similar number of loans, just 4 fewer defaults, and over twice my return). Lending Club consistently touts the returns of investors with over 800 notes – and even those with 400 notes are doing pretty well. Of course, high (or any) returns will never be guaranteed, which is why I’d never put in money I actually need, or expect to earn anything but the most basic of returns.

How about you – are you still using Lending Club? If so, share your experience in the comments!

I’ve been doing lending club for the past month, started with the incentive program and have enjoyed it so far, but not yet sure how I am going to do on earnings. I have over 900 notes and all are between $25 to $100 each. Hoping to do well and should hopefully find out more soon.

Wow that’s alot of loans for someone who has only been investing for a month! Did you feel like there were enough to choose from? Sometimes I can’t even find one or two I like on a given day!

My net return is published as 10.27%. Plus you can use the secondary trading platform to liquidate notes, often at a premium. I think the problem that you might be encountering is that you are not setting up proper screening for your notes. I invest in mostly C-F notes. I do have a small number of defaults but if you screen for deliquencies, home ownership, length of employment and DTI, etc, you should have considerably more success. I think I swiped my screening criteria from someone else online somewhere. I think lendingclub provides consistent returns and enough liquidity. I’ve been stashing my savings for property taxes (along with general savings) there and liquidate notes at a premium over the month before they’re due.

I had what I considered good screening criteria back in the day (I even wrote a post about it: https://www.mydollarplan.com/how-to-earn-high-returns-with-lending-club/). It seems like there is a certain amount of luck involved. I will say that I stopped investing consistently several months ago, so that has messed with my return – keeping the number high depends at least somewhat on continuing to reinvest your proceeds and/or adding new money.

I have been investing with Lending Club for about 10 months now. So far I have been reasonably happy with the returns, and the default / late payment rates I have experienced. When you compare this to other available investments it seems like a good choice.

However, it is not a “set it and forget it” type investment. Your payments are not automatically reinvested, unless you opt for their active management which is a 2% fee, which in my opinion takes this out of the money. Also, I have been un-successful in getting any takers on the trading side of the site. So it doesn’t appear to be as liquid as I once thought. So getting your money out may be a multi-month/year process.

Still I am reinvesting the proceeds at this time, but I wouldn’t put anything into this that I would think I would need to get out quickly.

Bottom line, it takes a fair amount of work to get these returns.

“All told, a full 10% of my loans have been charged off, and several more look to be headed that way. What’s frustrating is that there doesn’t seem to be a rhyme or reason to the charge-offs”

At least now you understand why credit card companies charge 19% interest and pay day loans companies charge such crazy fees since i assume their charge off rate is well over double yours and probably in to the 5 times yours.

The Credit card charge off rate is published.

http://www.federalreserve.gov/releases/chargeoff/

Seriously, filter your notes. I did this around three months ago and my defaults have dropped off dramatically. Even after adding a filter you can pick and choose and find some good returns!

I am, an with great returns. I’ve heard that after they went through the SEC registration, the average returns have gone up and the default rate has dropped significantly.

I’ve asked this in the past, but I never have gotten a clear-cut answer from anyone.

At the end of each year, do you get a tax form from Lending Club?

If so, what do you do with it when you file your tax return?

If not, how do you account for the interest you receive when you file taxes?

I’m not looking for a super-detailed answer, just a quick summary of the tax implications of P2P lending.

Thanks.

@Executioner

Details about tax is mentioned in the help section of the lendingclub website.

Summary : they will send 1099 at the end of the year and even if they don’t send one is supposed to declare just like any other fin instituion

Hi E,

Here’s the article that explains and details all of the Lending Club taxes: How Do You Handle Lending Club Taxes?

Nice, good info. Thanks for providing this link.

OID forms are a bit of a pain. The absence of a 1099 form at all is even more of a pain. Too bad tax reporting for Lending Club isn’t simpler. However, it may still be a worthwhile endeavor if the return is decent.

Thanks for the honest review and all of the great comments from people that have also had experience with social lending.

I wanted to get involved, but am not eligible based on which state I live in.

I have been investing in the Lending Club since 2009 and currently my Net Annualized Return is 7% on about $6000. I invest evenly in A, B, C,& D loans and am very satisfied with the program. The only thing that you have to remember is that the money can not be withdrawn quickly if needed.

Depends on how you define “quickly” & depends on whether you’re willing to accept a small discount in order to get out “quickly”. The liquidity is actually quite good. For various reasons I’ve sold over 400 notes in my almost 3 full yrs at LC. Early in 2011 when I was doing some re-balancing there was a 1 month period where I sold almost 120 notes, at a slight premium no less.

I would suggest starting with A notes or B notes at such a low balance. It’s possible to achieve a default rate of less than 2% at these grades.

I’ve been investing with Lending Club since March 2015 starting at $5000 at $25/loan. I used their auto selection to start the account and had several defaults immediately within a month! So I stopped investing in C-F notes. I’m surprised to hear so many people successfully investing in the high interest rate notes. I have <1% of my total in those notes and the defaults are significantly reducing my returns to 8.5%.