I want to explain to you the impact volatility has on investments. If you are unfamiliar with the term volatility, it can be defined as the fluctuation of value of the underlying asset. A government bond [1] fund is not very volatile. Its price does not swing wildly from one day to the next. On the other hand, a small company international fund [2], (or emerging markets fund) can be very volatile in price. Over time, this volatility can dictate the return you earn on your investments.

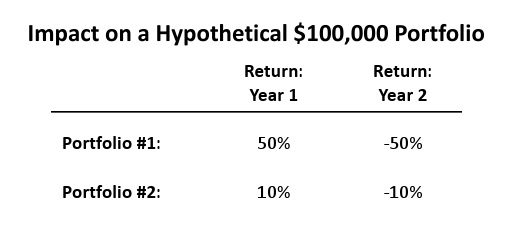

Which Investment Would You Choose?

Below I list two investments and their given return each year for two years. You have $100,000 but can only invest in one of the investments. Which one would you choose?

{kind=link}

Many people will see the 50% return in Portfolio #1 and choose that one. After all, a 50% return is much better than a 10% return. Others may see the increase in year one offset by the decrease in year two and think both portfolios have the same return after two years.

Would You Still Choose the Same Investment?

What if I gave you the scenario where you again have $100,000 and after two years of investing, you could have either $75,000 or $99,000. Which one would you choose? I’m hoping most would have picked the $99,000. Would it surprise you that the $99,000 is the value of Portfolio #2 from the example above? The $75,000 is the ending value of Portfolio #1.

The above is the reason why when choosing your investments, volatility matters. When calculating the returns on the above portfolios, both have an average return of 0% for two years. (Average return is calculated by adding up the two years returns and dividing by two). However, when we compound the returns, the return is -13.4% for Portfolio #1 and -0.5% for Portfolio #2. Why is this?

When you have $100,000 and earn a 50% return on your money, you just gained $50,000. If you then lose 50% of your money, you aren’t losing $50,000. You are losing 50% of the current value, $150,000. A 50% loss of $150,000 is $75,000. So while looking at the gain of 50% in year one and a loss of 50% in year two, one would assume that you end up with $100,000. But you don’t. You only have $75,000. The same holds true for Portfolio #2. It looks as though you have $100,000 after two years. But in reality you have $99,000.

How Do You Avoid Volatility?

Unfortunately, you cannot completely avoid volatility. In the short-term, there will be lots of volatility. It’s just the way it is. Over the long-term, volatility tends to lessen, but never truly goes away. But by having a well-diversified portfolio [3], you can down play stock market volatility. Investing in both an emerging market fund and a bond fund will help to cancel out some of the volatility that you will experience. This lessening of volatility will help you in the long run.

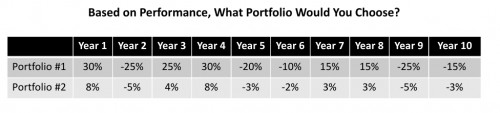

Let’s look again at two portfolios. Portfolio #1 is made up of highly volatile funds, while Portfolio #2 is a well-diversified portfolio. You see the annual returns for each one over the course of ten years. What is the value of $100,000 after ten years?

{kind=link}

For Portfolio #1 after ten years, your $100,000 turned into a little more than $96,000. For Portfolio #2, your $100,000 turned into just over $107,000. The point isn’t that the more volatile portfolio has a negative return. It just came out that way after putting the numbers together. The point is that after ten years of emotions that span the entire emotional spectrum from utter despair to exuberance, your $100,000 is still worth roughly $100,000. You could have saved all of that mental energy you wasted over the past ten years on this portfolio and instead invested in the other portfolio. Not only did you end up with a 7% return, you could have focused your mental energy on other areas of your life [4], such as your family or hobbies.

If we look at the annual returns, you will see what I am talking about. With Portfolio #2, the returns are fairly stable, not deviating too much. Contrast that with Portfolio #1 where it jumps up 30% one year only to fall 25% the next, then jumps back up again. It is basically a roller-coaster. Roller-coasters are great for the amusement park, not so much for investments.

If you are investing for the long-term, to be successful [5] you need to have a well-diversified portfolio. This portfolio will include higher volatility investments. But, as seen in the example above, you can limit some of the volatility over the long-term and experience healthy gains.

Which investment did you choose? Did your answer change after you understood how volatility impacted the overall return?