Today we’re wrapping up our Student Loan series with a look at exactly how much of a difference a few extra payments can make!

For many people, large amounts of student loan debt are the only thing standing in the way of being debt-free. Even if you choose the standard repayment option on a small-dollar non-consolidated loan, you will be making minimum payments for 10 years. In many cases, you can double the total loan amount when taking interest into account. If you take an extended repayment [1] option, your payments will be lower but your total amount paid will be even higher. Just like making extra payments [2] on a 30-year mortgage [3] can result in nearly the same results as a 15-year mortgage without the obligation, making larger payments on an extended or graduated plan can help bring your total payments closer to those of the standard repayment option. And making extra payments on a standard plan can mean student-loan freedom even faster.

Should you pay extra?

The largest argument for paying extra on your student loans is getting rid of debt and reducing the total amount of interest paid over time. Much like a mortgage, though, there are many reasons for not paying your loans off as soon as possible. For one thing, interest rates are typically low. Student loans should almost certainly be the last priority, except for maybe your mortgage, in any debt repayment plan [4]. Those making under $70,000 ($145,000 if filing jointly) receive a tax deduction [5] for student loan interest, so your student loan is actually costing you a little less to hold on to than you might think.

In a good interest rate environment, you might be paying less in interest than you would earn by parking your money in a high-interest savings [6] or money market [7] account. For instance, new loans right now have an interest rate [8] less than 5%, which some accounts used to earn and could again in the future. And those with a higher risk tolerance might choose to contribute more towards retirement and invest in stocks or bonds rather than pay down low-interest debt.

How fast you choose to pay off your loans depends on your personal circumstances as well as your attitude toward carrying debt.

Payment amount matters

If you do think that paying more than the minimum and zeroing out your student loans ahead of schedule may be for you, the following graphs might interest you. It’s amazing what even an extra $50 per month can do for debt eradication!

For these graphs, assume that a student has one loan for each of four years of college. To keep it simple, I assumed these were all subsidized and so no interest was accrued. The balances and interest rates at the start of repayment are as follows:

- $3,000 at 6%

- $4,000 at 6.2%

- $5,000 at 6.8%

- $5,000 at 4.5%

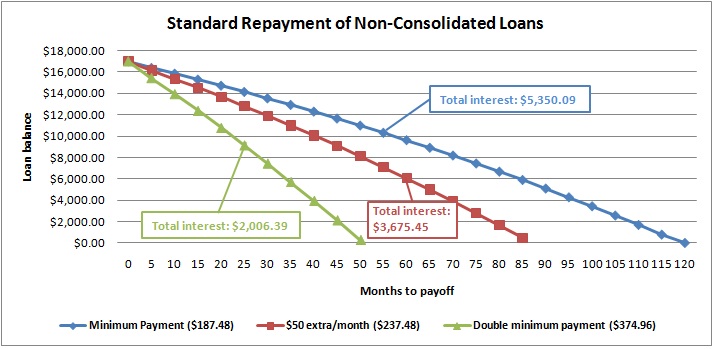

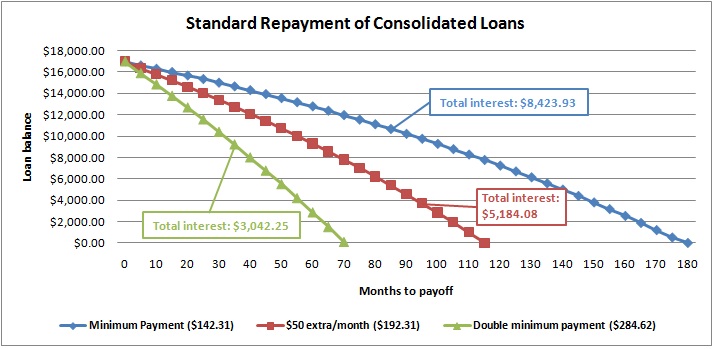

We looked at standard payments for consolidated and non-consolidated loans. For each payment option, we looked at paying the minimum, adding $50/month, and paying double the minimum.

{kind=link}

{kind=link}

As you can see, consolidating [9] your loans spreads the minimum payments out over 15 years rather than 10. If your loan amounts are higher, consolidating can actually spread payments out over as much as 30 years, significantly increasing the total amount of interest paid. Even in this case, paying minimum payments on consolidated loans can cost you about $3,000 than minimum payments on non-consolidated loans. And adding $50/month to your minimum payments saves you $3,000 on consolidated loans and about $1700 on non-consolidated loans. If you are fortunate enough to be able to double your minimum payments, you can pay off non-consolidated loans in just over 4 years! And doubling your consolidated minimum payment will still help you eliminate your student loans in less than half the expected time.

The bottom line: extra payments matter. If you can make them, do!

Check out all of the posts in our Student Loan series!

- Part 1: Student Loans: The Basics [10]

- Part 2: Student Loan Repayment Options [1]

- Part 3: Student Loans: Consolidation [9]

- Part 4: Student Loans: The Effect of Extra Payments [11]